There is a significant divide in how countries of the Eurozone’s north and south react to changes in monetary policy

Euro Crisis in the Press 2013-08-19

By Matteo Barigozzi

The European Central Bank (ECB) is charged with maintaining price stability across the Eurozone, which it does via its monetary policies. While the euro has had some success in smoothing out the asymmetries within the Eurozone, Matteo Barigozzi finds that when the ECB changes monetary policy, the Eurozone’s southern countries experience fluctuations in prices and unemployment outside of the Eurozone’s average. He argues that these differences are down to the structural and socio-economic traits of countries such as Portugal, Greece, and Italy. National reforms that are aimed at bringing regulations more in line with the countries of the Eurozone’s north will help to smooth out the current asymmetries.

The introduction of the euro in 1999 has been one of the major steps − if not “the” major step − towards European integration. Indeed, there is a debate on whether this is – or should be – the prologue to a more complete integration that, perhaps, could lead towards a United States of Europe.

The euro area (EA) is based on an hybrid structure that can be roughly described as follows: on the one hand the European Central bank (ECB) sets the common monetary policy based on euro area-wide goals (i.e., inflation close but below 2%), while, on the other hand, national governments set their own fiscal policies and design their regulation based on national goals and within the limits fixed by the European laws and the European Commission’s recommendations.

A necessary condition for this framework to be effective is that national economies respond similarly (or mostly similarly) to shocks that hit the whole area. Although one of the aims of, and one of the effects brought about by, the creation of the euro was to increase homogeneity across European economies, this has not been accomplished yet at a satisfactory level, as demonstrated by the recent global recessions that have revealed large asymmetries across countries.

While prior to the introduction of the common currency every euro area member state’s central bank had different goals, since 1999 the ECB has imposed a unique monetary policy. Nowadays, all EA countries are subject to this common policy, but are still characterised by different economic structures, legislations, fiscal policies, and levels of public debt. Such a diversified environment makes the ECB decision process particularly challenging as member states’ reaction to its policies might be different from country to country. It is then natural to ask whether, and to what extent, the EA countries respond asymmetrically to the common monetary policy decided by the ECB.

In order to answer this question we carried out a statistical analysis of the economies of euro area member states from 1983 to the end of 2007, along with colleagues* from the Université libre de Bruxelles and the Bank of Italy. The research incorporates data on 237 country-specific key economic variables, such as the gross domestic product, inflation, unemployment, consumption, investment, exports, imports and many others. In order to answer our research question, we simulated the effect of an unanticipated raise of 50 basis points in the reference rate set by the ECB, on the GDP, Consumer Prices Inflation and unemployment rate of different countries. By comparing these effects we were able to determine whether they were similar or not.

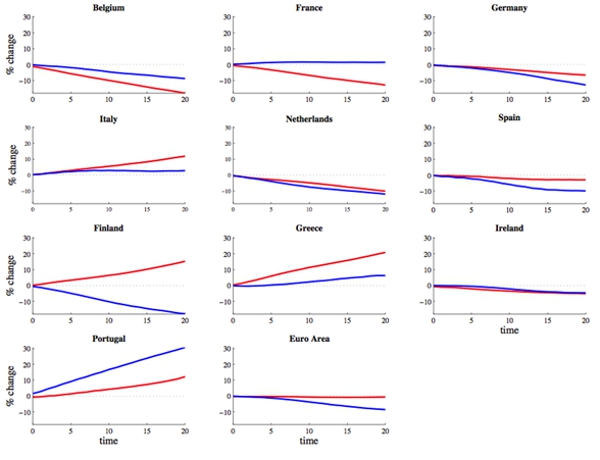

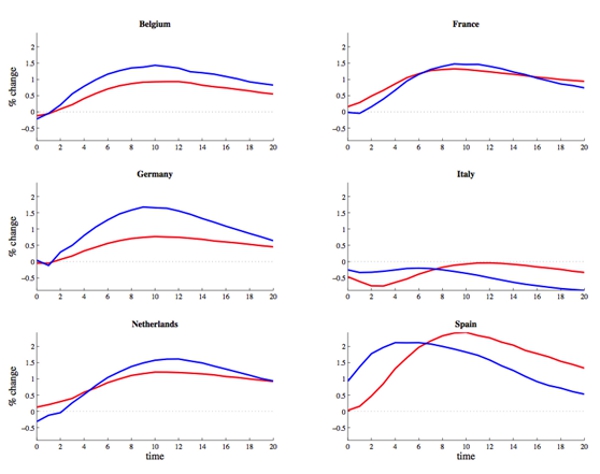

According to economic theory, an increase in the interest rate should make prices and output decrease while increasing unemployment. We found that EA countries react differently to the common monetary policy in terms of prices (as shown in Figure 1 below) and unemployment (as shown in Figure 2 below), while no difference appears in terms of output. However, we also found that the introduction of the euro, shown by the blue line in both Figures, has mitigated these differences. We believe that these differences have an idiosyncratic nature, and hence they can hardly be controlled by means of the common monetary policy; rather, they should be addressed by means of national fiscal policies, regulation, and structural reforms.

Figure 1: Reaction of CPI to an increase in ECB interest rate

Notes: Blue lines are the estimated reactions for the 1999:Q1–2007:Q4 (euro) subsample. Red lines are the estimated reactions for the 1983:Q1–1998:Q4 (pre-euro) subsample.

For example, the asymmetries in labour markets seem to be the result of structural and socio-economic characteristics of single countries. This is the case with the rigid labour market structure in Italy, which makes Italian unemployment rate unresponsive to the single monetary policy, as shown in Figure 2 below. Similarly, and not surprisingly, the remaining differences in terms of prices are observed in the Mediterranean countries, which historically have less flexible prices and lack of market competition.

Figure 2: Reaction of Unemployment Rate to an increase in ECB interest rate

Notes: Blue lines are the estimated reactions for the 1999:Q1–2007:Q4 (euro) subsample. Red lines are the estimated reactions for the 1983:Q1–1998:Q4 (pre-euro) subsample.

Notwithstanding the positive effects of the introduction of the euro, differences still remain between North and South Europe in terms of prices and unemployment. Although the post-1999 reduction in asymmetries is consistent with the aims of the ECB, the remaining differences are beyond the scope of monetary policy, and they should be addressed by means of national reforms. Out of their intrinsic interest, these results should sound as an alarm bell for the EA and should push towards greater integration and homogenization in the regulations. If this will not happen, we will continue to witness different responses of European countries to shocks hitting the whole area.

The euro area, though, is not sustainable if these asymmetries persist, since handling them is difficult from both an economic and a political point of view. As demonstrated by the recent/current public debt crisis, and by the skyrocketing of government bond spreads, these differences pose a threat to the region’s stability: addressing them is fundamental for the future of Europe, and it should be a priority if economic cohesion is to be achieved.

* Antonio M. Conti of the Bank of Italy and Matteo Luciani, ECARES, Université libre de Bruxelles also contributed to this research.

This article first appeared on the LSE EUROPP blog and is based on a longer paper, Do Euro Area Countries Respond Asymmetrically to the Common Monetary Policy?

____________________

Matteo Barigozzi is a Lecturer in Statistics at the London School of Economics and Political Science and has a PhD in Economics from Sant’Anna School of Advanced Studies in Pisa.

Matteo Barigozzi is a Lecturer in Statistics at the London School of Economics and Political Science and has a PhD in Economics from Sant’Anna School of Advanced Studies in Pisa.